January 29, 2026

•

5 min read

The Super Peso: Why Mexico's Strong Currency Has Expats Nervous (And Why 2026 Is Different from 1994)

The Mexican peso has strengthened to 17:1 against the dollar, leaving many expats worried about a repeat of the 1994 "Tequila Crisis." Here's why today's peso operates on completely different machinery, and what risks you should actually be watching.

Justin Barsketis

Insurance Expert

Interested in expat health insurance? Click here for a 1-minute quote!

The Super Peso - Introduction

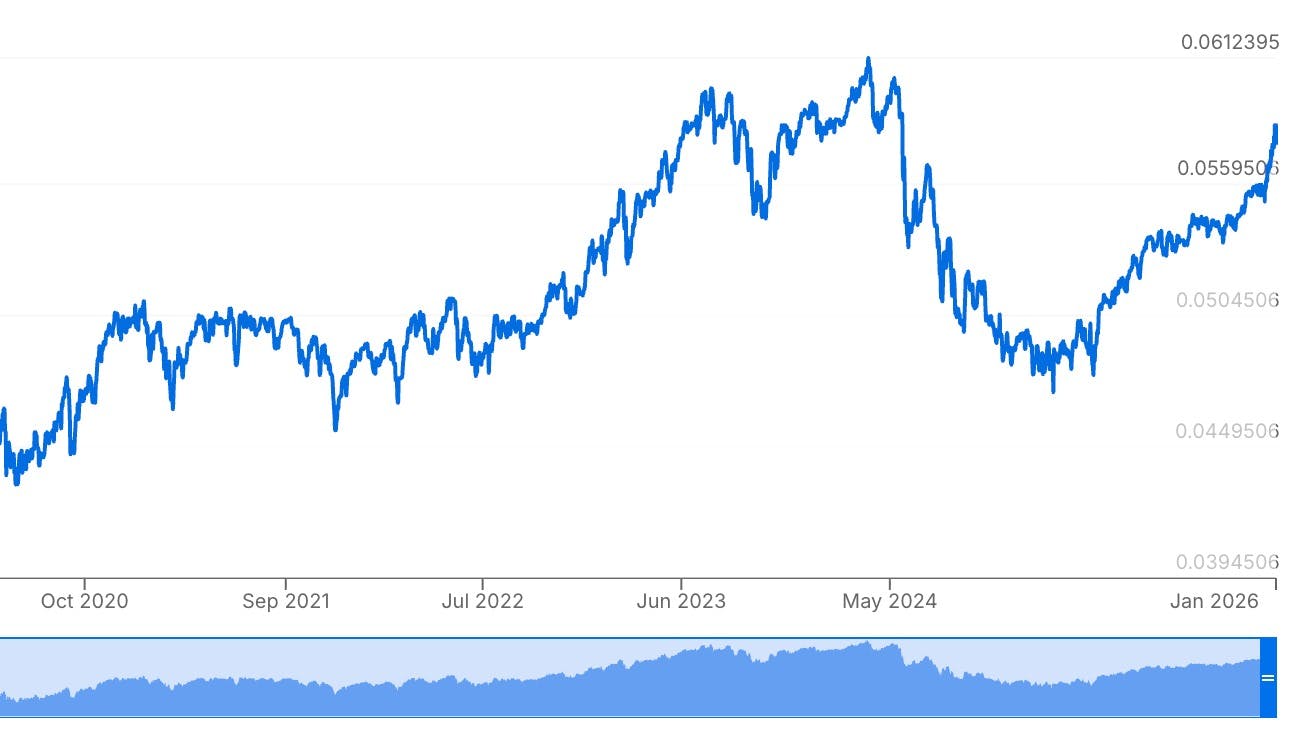

If you've been in Mexico long enough, you have a kind of muscle memory for peso devaluation. You expect the chart to go up and to the right. More pesos for your dollar. That's just how it works.

So when the exchange rate starts creeping back toward 17:1 (and recently dipping below it), something feels off. For those of us living on dollar income, this isn't an abstraction. It's a pay cut. Your $3,000 monthly transfer that used to net 60,000 pesos now gets you 51,000. That's real money missing from your grocery budget, your rent, your life.

We hear the same question constantly from clients and fellow expats: "Should I wait to transfer my money? Won't the peso crash eventually?"

To answer that honestly, we need to talk about the ghost that haunts every conversation about Mexican currency. We need to talk about December 1994.

The Super Peso - The Tequila Crisis: What Actually Happened

In financial circles, they call it the "Tequila Crisis." In Mexico, it's simply El Error de Diciembre. The December Mistake.

This single event is why, for the past 30 years, conventional wisdom among expats and locals alike has been: "Keep your savings in dollars. The peso always crashes eventually."

Here's what actually happened.

- The Setup: Artificial Stability -

In early 1994, Mexico looked like a success story. NAFTA had just taken effect on January 1st. Inflation was finally under control. The peso was trading around 3.1 to the dollar and holding steady.

But that stability was artificial. The government was running what's called a "crawling peg" system. Instead of letting the market determine the peso's value, the central bank promised to keep it within a narrow price band. Every time the peso wobbled, they burned through foreign currency reserves to prop it up.

Think of it like a dam holding back water. As long as you have enough sandbags, everything looks fine. But the pressure keeps building.

- The Fatal Flaw: Dollar-Denominated Debt -

Then 1994 turned ugly. In March, presidential candidate Luis Donaldo Colosio was assassinated in Tijuana. In September, another political murder. Investors got spooked and started pulling money out.

To convince them to stay, the government made a fateful decision. They issued a special type of bond called Tesobonos. The deal was simple: you buy this bond in pesos, but we'll pay you back in dollars.

The risk should have been obvious. If the peso crashed, the government's debt burden would explode overnight because they'd need far more pesos to cover the same dollar amount.

By December, Tesobono debt had ballooned from $3 billion to $29 billion in just nine months. It went from 6% of government debt to 50%. And the central bank's dollar reserves were nearly empty.

- The Crash -

On December 20, 1994, the new administration admitted defeat. They tried a controlled 15% devaluation. It failed immediately. Within two days, they abandoned the peg entirely and let the peso float.

Investors didn't walk away. They ran.

The peso went from 3.46 to 5.50 in just two days. By March 1995, it had fallen to 7.20. A Mexican salary that bought 100 items at the grocery store in November could only buy 50 by spring. Businesses with dollar loans owed double what they'd borrowed, overnight.

- The Aftermath -

The numbers from 1995 still shock. Inflation hit 52%. The bank lending rate topped 59%. Credit card rates likely exceeded 100% for many borrowers. People lost homes and cars because they couldn't pay the interest, let alone the principal.

The US Treasury organized a $50 billion emergency bailout. Mexico repaid it early and the US actually made $600 million in profit on the deal. But that doesn't erase the trauma.

For a generation of Mexicans and expats, this became the defining lesson about the peso: It's a ticking time bomb.

And that's why, 30 years later, a strong peso makes people nervous. They're not looking at today's economic data. They're remembering December 1994.

The Super Peso - Why 2026 Is Actually Different

Here's the thing: the Mexican economy today operates on completely different machinery than the one that blew up in 1994. There are three structural changes that make a repeat of that crisis highly unlikely.

- The Float: No More Hidden Pressure -

Since December 22, 1994 (two days after the initial devaluation), the peso has been a free-floating currency. The government doesn't set the price anymore. Supply and demand do.

This matters enormously. In 1994, pressure built up behind the dam in secret. When it broke, the flood was catastrophic.

Today, when bad news hits (tariff threats, election uncertainty, a controversial statement), the peso adjusts immediately. It might drop from 17 to 18, then recover to 17.50. The volatility you see on the screen is actually a safety feature. It's the pressure releasing in real time instead of building toward an explosion.

The peso is now one of the most actively traded emerging market currencies on the planet. That liquidity provides stability that simply didn't exist 30 years ago.

- The Carry Trade: Getting Paid to Hold Pesos -

This is the main financial reason the peso has been so strong.

Right now, Mexico's central bank (Banxico) pays 7.00% on overnight deposits. The US Federal Reserve's target range is 3.50% to 3.75%. That 325+ basis point spread is attractive to global investors.

The trade works like this: borrow money cheaply in dollars, convert it to pesos, park it in Mexican instruments, and pocket the difference. As long as the peso doesn't depreciate faster than the yield advantage, you make money. This creates constant demand for pesos from institutional investors around the world.

The contrast with 1994 is stark. Back then, the government was issuing dangerous dollar-denominated debt (Tesobonos) to beg investors to stay. Today, investors are choosing to be here because an independent central bank has kept rates high enough to make it profitable.

- Nearshoring: Sticky Money vs. Hot Money -

In the 1990s, foreign money in Mexico was mostly speculative. Portfolio investors buying stocks who could click "sell" and disappear in seconds. That's called "hot money" for a reason.

The peso strength we're seeing now is driven by something much harder to move: factories.

Mexico received over $40 billion in foreign direct investment through September 2025, already exceeding the full year 2024 total. Q1 2025 alone set an all-time record at $21.4 billion. Amazon Web Services committed $5 billion for data centers. Microsoft put in $1.3 billion for AI infrastructure. Japanese auto suppliers have pledged $18 billion.

When BMW builds a plant in San Luis Potosí, they're not buying stocks. They're buying land, pouring concrete, installing equipment, and hiring thousands of workers. You can't liquidate a factory with a phone call because you got nervous about a headline.

This is "sticky money." It creates a genuine, long-term floor for peso demand that didn't exist in the speculative 1990s.

- The Bottom Line on Structure -

In 1994, the peso was a house of cards held up by government promises and dwindling reserves. In 2026, it's a globally traded currency backed by an independent central bank, attractive interest rates, and tens of billions in physical infrastructure investment.

Will it stay at 17 forever? No. Could it weaken to 19 or 20? Absolutely. But a 1994-style overnight collapse where you wake up and half your purchasing power has evaporated? The structural conditions for that simply don't exist anymore.

The Super Peso - The Real Risks for 2026

So should you convert your life savings to pesos and call it a day?

Absolutely not.

The structural crash risks of 1994 are gone, but that doesn't mean the peso faces smooth sailing. There are real headwinds gathering that could push the rate back toward 19 or 20. If you're living on dollar income, these are the storm clouds worth watching.

- The Interest Rate Spread Is Shrinking -

Remember that carry trade? It only works as long as Mexican rates stay significantly higher than US rates.

Banxico has been cutting rates steadily since March 2024. We've seen 12 consecutive cuts, bringing the rate from 11.25% down to 7.00%. Bank of America expects it to hit 6.00% by the end of 2026.

Meanwhile, the Fed has been slower to cut. If that spread narrows from 325 basis points to, say, 200, some of that "easy money" will flow elsewhere. Less demand for pesos means a weaker peso.

- The USMCA Review in July -

Mark your calendar: July 1, 2026.

That's the mandatory six-year review of the USMCA trade agreement. Under the treaty, all three countries must decide whether to extend it for another 16 years. If any party declines, the agreement enters a slow death spiral of annual reviews until it expires in 2036.

The review process has already started, and the signals from Washington are not reassuring. US Trade Representative Jamieson Greer said in December 2025: "Could it be exited? Yes. Could it be revised? Yes. Could it be renegotiated? Yes. All of those things are on the table."

The biggest friction point is Chinese companies using Mexico as a backdoor to the US market. Chinese FDI in Mexican auto parts and electrical equipment rose 77% through May 2025. Mexico's imports from China hit $130 billion, with a trade deficit of $120 billion. Washington sees this as tariff evasion, and they're not wrong.

Mexico has tried to get ahead of this by imposing tariffs up to 50% on Chinese goods effective January 2026. But whether that's enough to satisfy US concerns remains unclear.

Every time a US Senator threatens new tariffs or a trade dispute makes headlines, algorithms will sell pesos. Expect volatility as we approach July.

- Remittances: The First Crack -

This one hasn't gotten enough attention.

Remittances to Mexico hit a record $64.7 billion in 2024. That's more than double Mexico's oil export revenues and represents the 11th consecutive year of growth. About 1.8 million Mexican households depend on this money.

But in 2025, the streak broke. First-half remittances fell 5.6% year-over-year. June 2025 alone plunged 16.2%, the biggest monthly drop in a decade.

The likely cause: immigration enforcement. An estimated 4.3 million unauthorized Mexican workers in the US are sending less money home, either because they're earning less or because they're afraid of drawing attention to themselves.

On top of that, Mexico implemented a 1% tax on cash remittances starting January 1, 2026. That's not huge, but it's another headwind.

Remittances represent 3-4% of GDP. If this decline continues, it removes a significant source of dollar-to-peso conversion that has been supporting the currency.

- The Pemex Problem -

Pemex is the most indebted oil company on the planet. About $100 billion in financial debt, plus another $28 billion owed to suppliers. Oil production has fallen 28% over the past decade.

The Mexican government keeps Pemex alive through direct support. That's a big reason the fiscal deficit hit 5.7% of GDP in 2024 (a 36-year high) and is projected at 4.1% for 2026.

Credit rating agencies are watching. Moody's changed Mexico's outlook to "negative" in November 2024, citing fiscal deterioration and Pemex liabilities. Fitch rates Mexico just one notch above junk status.

A sovereign credit downgrade wouldn't cause an overnight crash. But it would raise borrowing costs, spook some of that sticky FDI money, and put downward pressure on the peso.

- Tariffs Are Already Here -

This isn't a hypothetical future risk. Tariffs on Mexican goods are already in effect. There's a 25% tariff on goods that don't meet USMCA requirements (since February 2025), a 50% tariff on steel and aluminum (raised from 25% in June 2025), and a 25% tariff on automobiles and auto parts not meeting USMCA content rules.

USMCA-compliant goods remain exempt, which is why the nearshoring investment continues. But the trade relationship is clearly more fraught than it was even two years ago.

- What the Analysts Say -

The January 2026 Citi México survey of 35 banks forecasts the peso at 18.75 to 19.00 per dollar by year-end. Forecasts range from 17.10 (XP Investments, most bullish) to 20.30 (Banca Mifel, most bearish).

The bull case (peso stays 16.50-17.50) assumes nearshoring continues, the US economy avoids recession, and the USMCA review goes smoothly. The bear case (peso weakens to 19-20) assumes USMCA talks turn hostile, the carry trade unwinds faster than expected, or a US recession crushes export demand.

The Super Peso - What This Means for Your Money

Nobody can predict currency movements reliably. Not us, not Wall Street, not the algorithms. Anyone who tells you they know where the peso will be in six months is either lying or selling something.

What we can tell you is how to think about it.

- Stop Trying to Time the Market -

If you're waiting to transfer money until the peso hits 20, you might be waiting a very long time. Or it might happen next month. That's the point: you don't know, and neither does anyone else.

Don't delay important decisions (buying property, paying for insurance, making investments) because you're hoping for a better rate. Make decisions based on your actual needs and timeline.

- Budget for the New Normal -

If your lifestyle in Mexico only works at 19:1 or 20:1, you're financially vulnerable. Build your budget assuming 17:1 as the baseline. If it weakens, treat the extra pesos as a bonus, not a requirement.

This might mean hard choices: a smaller apartment, fewer restaurant meals, reconsidering that second car. Better to make those choices deliberately than to have them forced on you by currency movements. For more on managing your cost of living in Mexico, check out our detailed guide.

- Diversify Your Currency Exposure -

Don't keep 100% of your liquid savings in one currency if you have expenses in both. Yes, you'll miss some upside if the peso weakens dramatically. But you'll also be protected if it doesn't.

Some practical approaches: maintain accounts in both currencies, consider dollar-denominated investments for long-term savings, and keep your emergency fund in the currency of your largest fixed expenses.

- Lock in Dollar-Denominated Protection -

Your grocery bill will fluctuate with the peso. Your rent might be negotiable. But a medical emergency shouldn't depend on what the exchange rate happens to be that week.

International health insurance plans are typically priced in USD. That means your coverage level stays constant regardless of peso movements. When you need to be evacuated or hospitalized, you're not also dealing with the stress of currency math.

The Super Peso - The Silver Lining

A strong peso isn't all bad news, even for those of us paid in dollars. It typically signals a stable local economy, controlled inflation, and property values that hold their worth. The businesses you frequent can afford to import goods and keep their doors open. The infrastructure investments happening around you will likely continue.

The ghost of 1994 is real. The trauma it caused shaped how a generation thinks about Mexican currency. But the Mexico of 2026 runs on different machinery. The old rules don't quite apply anymore.

Budget conservatively, diversify sensibly, and stop checking the exchange rate every morning. Your blood pressure will thank you.

Frequently Asked Questions About the Super Peso

Will the peso crash like it did in 1994?

A 1994-style crash is highly unlikely due to structural changes: the peso now floats freely (no artificial peg), Mexico has an independent central bank, and foreign investment is "sticky" (factories and infrastructure) rather than "hot money" (speculative stocks). While the peso could weaken to 19 or 20, an overnight collapse of 50% is not in the cards.

Why is the peso so strong right now?

Three main factors: high interest rates from Banxico (7.00% vs. US rates of 3.50-3.75%) attract global investors through the "carry trade," massive nearshoring investment from companies building factories in Mexico, and Mexico's position as a key US trading partner under USMCA.

Should I wait to transfer my dollars until the peso weakens?

Trying to time currency markets is a losing game. If you need pesos for expenses, transfer based on your actual needs, not predictions. Budget assuming 17:1 and treat any weakness as a bonus rather than an expectation.

What could cause the peso to weaken in 2026?

Key risks include: the USMCA review in July 2026, shrinking interest rate spreads as Banxico cuts rates, declining remittances (down 5.6% in first-half 2025), Pemex debt concerns, and ongoing tariff tensions with the US.

How should expats protect themselves from currency fluctuations?

Diversify your currency exposure by keeping accounts in both dollars and pesos, budget conservatively at current rates, and consider dollar-denominated insurance and investments for protection against peso weakness.

Related Articles:

- Tips for Bringing and Spending Money in Mexico

- Cost of Living in Mexico

- Americans Can Open a Bank Account in Mexico

- Buying Property in Mexico

- What Is a Fideicomiso?

- Avoid International Fees with Smart Banking

- Who Was Luis Donaldo Colosio?

Justin Barsketis

Insurance Expert & Writer

Justin is an insurance guru that loves digital marketing. As our founder Justin manages our business development programs and MGA network. Please don’t hesitate to contact him if you are not getting the attention you deserve.