December 14, 2025

•

5 min read

What Is Out of Pocket Maximum? Your Guide to Health Insurance

Confused about what is out of pocket maximum? This guide simplifies health insurance costs, deductibles, and what counts toward your limit with clear examples.

If you’ve ever tried to make sense of a health insurance policy, you’ve probably felt like you’re learning a whole new language. Between deductibles, copays, and premiums, it's easy to get lost in the jargon. But there’s one term that, above all others, you absolutely need to understand: the out-of-pocket maximum.

Think of it as your financial safety net. It’s the absolute most you’ll have to pay for covered medical services in a single year. Once you hit this limit, your insurance plan steps in and pays for 100% of all covered costs for the rest of the policy year. No more bills, no more surprises—just peace of mind.

Your Financial Safety Net In Health Insurance

This number is arguably the most important one on your entire policy because it puts a hard ceiling on your annual medical spending. It’s what protects you and your family from truly catastrophic bills that could otherwise lead to financial ruin.

This concept is so critical for consumer protection that many governments regulate it. In the United States, for example, the Affordable Care Act (ACA) sets annual limits on these maximums to keep healthcare costs from spiraling out of control for individuals and families.

Why This Number Matters For Expats

For expats, global nomads, and anyone living abroad, understanding your out-of-pocket maximum is even more critical. When you’re choosing an international health plan, this figure directly translates to your total financial risk in a foreign country.

Your out-of-pocket maximum transforms healthcare from a potentially unlimited financial liability into a predictable, budgetable expense. It is the ultimate line of defense for your savings in a medical emergency.

This guide will break it all down for you, piece by piece. We're going to demystify this crucial part of your insurance so you can feel confident in your coverage. We'll cover:

- What kinds of costs actually build toward your limit.

- Which expenses count and, just as importantly, which ones don't.

- A real-world example showing how it all works in practice.

- Smart strategies for picking a plan that matches your personal risk tolerance.

To really get the most out of your plan, it helps to know the fundamentals. Make sure you grasp the key differences between travel insurance vs health insurance, as they serve very different purposes. And if you're planning your move, our guide on securing health insurance when living abroad is a must-read.

By the time you're done here, you’ll see the out-of-pocket maximum not as confusing jargon, but as a powerful tool for your financial security.

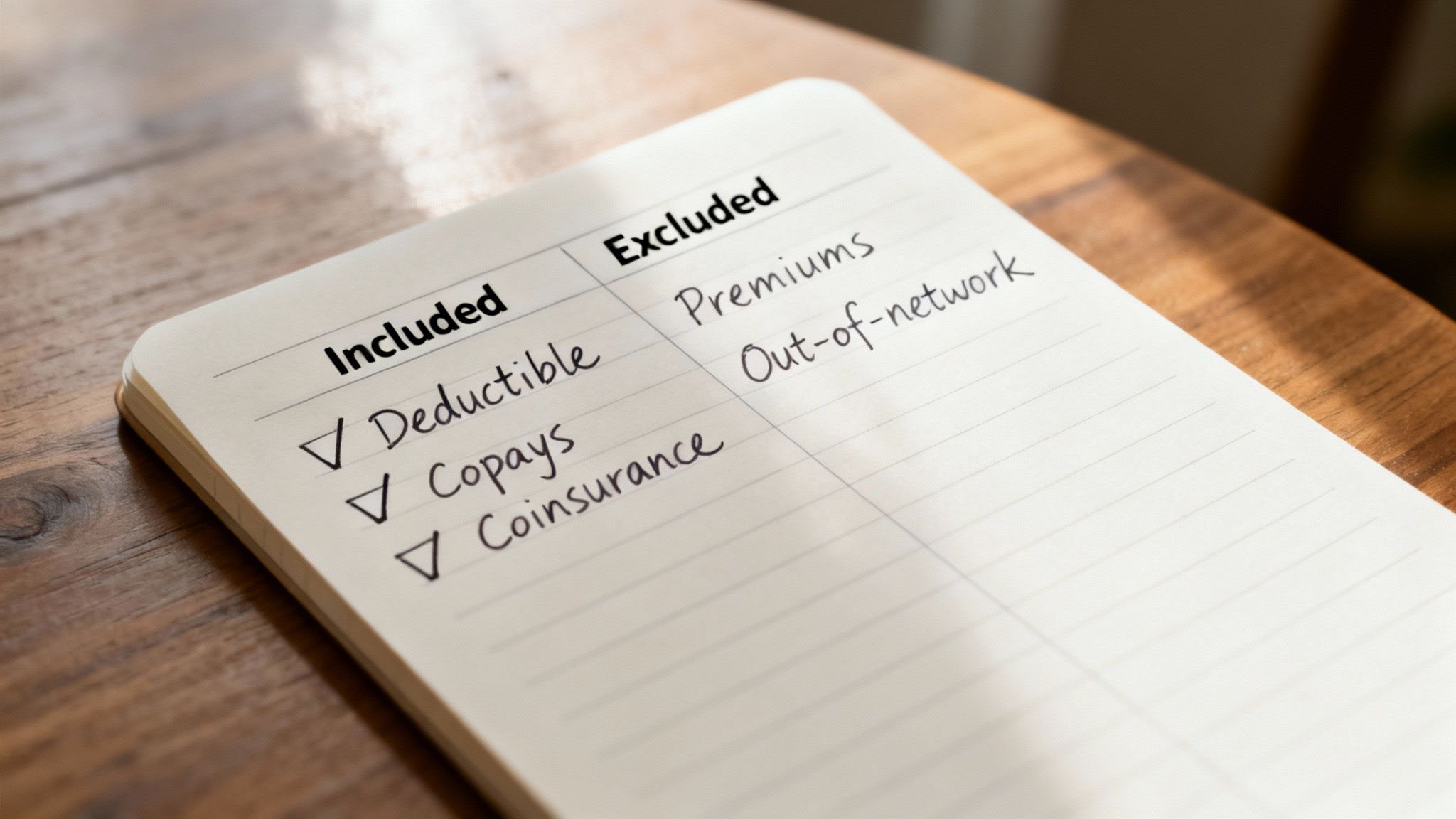

Key Health Insurance Costs at a Glance

Before we dive deeper, let's get a quick lay of the land. This table helps sort out the different terms you'll encounter and how they relate to your out-of-pocket max.

| Term | What It Is | How It Contributes to Your OOP Maximum |

|---|---|---|

| Deductible | The amount you pay for covered services before your insurance starts paying. | Yes, payments toward your deductible typically count. |

| Copayment | A fixed fee you pay for a specific service, like a doctor's visit. | Yes, copayments for in-network, covered services count. |

| Coinsurance | The percentage of costs you pay for a service after you've met your deductible. | Yes, your coinsurance payments count toward the maximum. |

| Premium | The fixed monthly or annual amount you pay to keep your insurance active. | No, your premiums almost never count toward the maximum. |

| Out-of-Pocket Max | The absolute most you'll pay for covered care in a year. | This is the finish line! Once you hit it, insurance pays 100%. |

Think of these terms as building blocks. Each time you pay a deductible, copay, or coinsurance, you’re adding another block to the tower. Once that tower reaches the height of your out-of-pocket maximum, you’re done building for the year.

Breaking Down Your Core Health Insurance Costs

To really get a handle on the out-of-pocket maximum, you first have to understand the four main pieces of your health plan's cost puzzle. Each one has a specific job, but only three of them actually help you reach that all-important spending cap for the year.

The first and most familiar cost is your premium. This is the non-negotiable fee you pay every month or year just to keep your insurance policy active. Think of it like a subscription service—you pay it whether you use the benefits or not.

Here’s the most important thing to remember about premiums: they do not count toward your out-of-pocket maximum. Your premium is simply the cost of admission. The real countdown to hitting your limit only starts once you actually start using your healthcare benefits.

The Costs That Count

The real players in this game—the ones that get you closer to your out-of-pocket limit—are your deductible, copayments, and coinsurance. These are the direct costs you pay when you see a doctor, fill a prescription, or have a medical procedure.

First up is the deductible. This is the amount you have to pay out of your own pocket for covered medical services before your insurance company starts chipping in. To get the full story on this initial hurdle, check out our guide to understanding health insurance deductibles.

Once you’ve met that deductible, your insurer starts sharing the cost. That’s where the other two pieces come into play.

- Copayments (Copays): This is a simple, flat fee you pay for a specific service. You might have a $30 copay for a routine check-up or a $100 copay if you have to visit the emergency room. It’s predictable.

- Coinsurance: This is your share of the costs after your deductible is met, expressed as a percentage. If your plan has 20% coinsurance, you’ll pay 20% of the approved medical bill, and your insurer covers the remaining 80%.

Every single dollar you spend on your deductible, copays, and coinsurance for in-network services adds up, bringing you one step closer to reaching your out-of-pocket maximum.

How Federal Rules Shape Your Maximum

The out-of-pocket maximum isn't just a helpful feature; it’s a critical consumer protection, especially in the United States. Before the Affordable Care Act (ACA) was passed in 2010, there was no federal cap on what you could be asked to pay. This left people facing the terrifying possibility of unlimited medical debt.

The establishment of annual out-of-pocket maximums transformed health insurance, creating a predictable ceiling on medical spending and protecting families from financial devastation.

Today, the government sets limits that are adjusted each year. For 2025, ACA marketplace plans will have maximums of $9,200 for an individual and $18,400 for a family. This shows just how directly government policy can impact your financial safety net, ensuring there’s a clear and defined end to your medical spending in a given year.

What Actually Counts Toward Your Out of Pocket Maximum

Knowing what an out-of-pocket maximum is is only half the battle. The real trick is knowing exactly which expenses actually chip away at that limit.

This is a detail that trips up a lot of people and can lead to some nasty, expensive surprises. Not every dollar you spend on healthcare pushes you closer to that financial safety net.

Think of it like a special kind of savings account. Only certain deposits count toward your goal, and if you aren’t putting in the right kind of money, it won’t add up. To really get a handle on this, you have to dig into the details of your plan, which includes understanding the fine print on excesses and deductibles.

The Costs That Count

In pretty much any health plan, the only spending that will count is your direct payment for covered, in-network medical services. These are the building blocks that stack up to eventually hit your maximum.

- Your Deductible: This is the first big one. Every dollar you put toward your annual deductible for covered services gets you one dollar closer to your out-of-pocket max.

- Your Copayments: Each of those fixed fees you pay for a doctor’s visit, specialist appointment, or trip to the emergency room—like a $40 copay—gets added to your running total.

- Your Coinsurance: Once you’ve met your deductible, your share of the costs for procedures and services also counts. That 20% you pay for a hospital stay directly lowers what's left before you hit the limit.

Basically, if the service is covered, the doctor is in-network, and you’re paying for part of it directly, it should count.

Common Expenses That Do Not Count

Just as crucial is knowing what doesn't count. These are the expenses you’ll keep paying no matter how much you’ve spent on other medical bills. Getting this part wrong is how unexpected bills show up.

The most common mistake people make is assuming their monthly premiums count toward the out-of-pocket maximum. They don't. Premiums are simply the price of admission to keep your insurance active; they are completely separate from your medical spending.

Here’s a quick breakdown of what’s almost always excluded:

- Monthly Premiums: As mentioned, this is just the fee for having coverage. It will never apply to your maximum.

- Out-of-Network Care: Going to a doctor or hospital outside your plan’s approved network? Those costs typically won't count. Some plans have a separate (and much higher) out-of-pocket max for this, while others won't cover it at all.

- Services Your Plan Doesn't Cover: Any treatment your insurer doesn’t consider medically necessary or that's explicitly excluded (like most cosmetic surgery) won't count. You’re on your own for those bills.

- Balance Billing Charges: This happens when an out-of-network provider charges more than what your insurance agrees is a fair price. The difference they bill you for—known as balance billing—doesn’t count toward your in-network maximum.

The best rule of thumb? Always double-check that a provider is in your network and a service is covered before you get care. That's the surest way to make sure every dollar you spend is actually working toward hitting your financial limit.

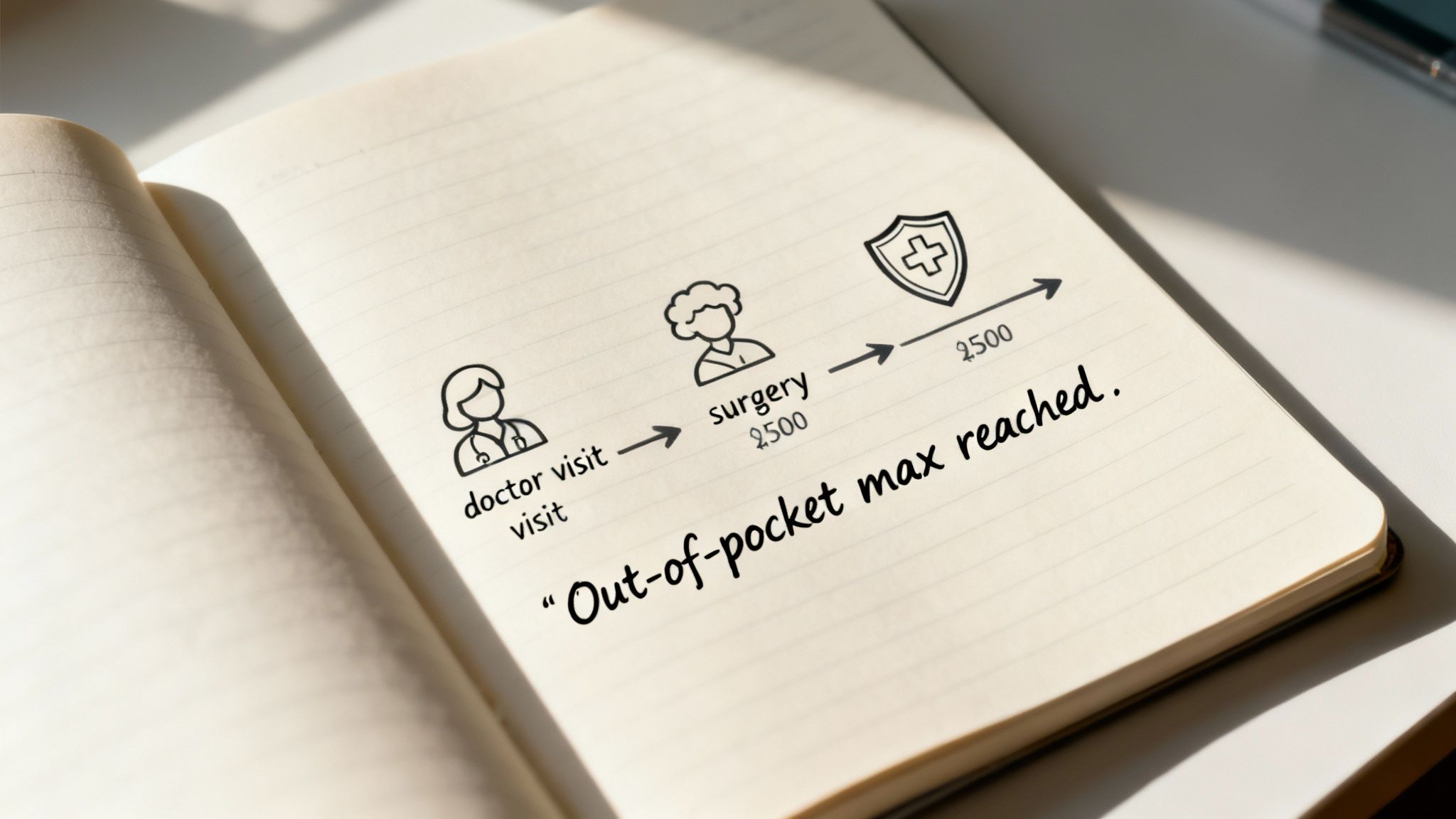

A Real-World Medical Cost Scenario

Insurance jargon can feel a bit abstract. All those numbers and terms don't really click until you see them in action. So, let's walk through a year in the life of a fictional expat named Alex to make the out-of-pocket maximum crystal clear. We'll watch how each medical bill adds up and pinpoint the exact moment that financial safety net kicks in.

Let's imagine Alex has an international health plan with these key figures:

- Deductible: $3,000

- Coinsurance: 20% (Alex pays 20% of the bill, the insurer pays 80%)

- Out-of-Pocket Maximum: $7,000

These are the only numbers we need to worry about for now. Remember, the monthly premiums Alex pays to keep the insurance active don't count toward any of these limits.

Starting The Year With Routine Care

The year starts off pretty normal for Alex. In February, a minor bug leads to a visit with an in-network doctor. The bill for the consultation and a few lab tests comes to $500.

Since it's early in the year, Alex hasn't paid anything toward the deductible yet. That means the entire $500 is Alex's responsibility. This single payment does double duty: it goes toward meeting the $3,000 deductible and it's the first contribution toward the $7,000 out-of-pocket maximum.

An Unexpected Major Medical Event

Then, in May, life throws a curveball. Alex has an accident that requires emergency surgery and a hospital stay. This is exactly the kind of high-cost situation where an out-of-pocket maximum proves its worth. The total approved bill for everything is a staggering $50,000.

Now the math gets interesting. Alex had already paid $500, so there was still $2,500 left to pay on the deductible ($3,000 total - $500). So, the first $2,500 of this new bill goes straight to satisfying the rest of the deductible. With that payment, the deductible is officially met for the year.

Once the deductible is met, coinsurance kicks in. The remaining cost of the surgery is $47,500 ($50,000 - the $2,500 Alex just paid). Alex’s share is 20% of that amount, which calculates to $9,500.

But here’s the critical part: Alex doesn't actually pay that full $9,500. The out-of-pocket maximum acts as a hard stop on spending.

So far, Alex has paid a total of $3,000 ($500 for the first doctor's visit + $2,500 to finish the deductible). The out-of-pocket limit is $7,000, which means Alex only has $4,000 left to pay before hitting that ceiling.

Alex pays $4,000 of the coinsurance bill, and at that moment, the financial protection activates. For the rest of the policy year, the insurance company pays 100% of all covered, in-network medical costs. The other $5,500 of that coinsurance bill? It's now the insurer's problem.

Let's break down how Alex's costs stacked up over the year.

Alex's Journey to the Out-of-Pocket Maximum

| Medical Service | Total Cost | Alex Pays | Amount Applied to Deductible | Amount Applied to Out-of-Pocket Max |

|---|---|---|---|---|

| February Doctor Visit | $500 | $500 | $500 | $500 |

| May Surgery (Part 1) | $50,000 | $2,500 | $2,500 (Deductible Met) | $2,500 |

| May Surgery (Part 2) | (Remaining $47,500) | $4,000 | N/A | $4,000 (OOP Max Met) |

| Yearly Totals | $50,500 | $7,000 | $3,000 | $7,000 |

As you can see, once Alex paid a cumulative $7,000, the personal spending stopped, even though there were more bills to come.

This protection is especially vital for anyone facing a serious, ongoing illness. For instance, someone undergoing cancer treatment might hit their deductible and out-of-pocket maximum very quickly. After that, the insurer covers all subsequent covered care for the year. You can get a deeper look at how out-of-pocket limits work in different health scenarios.

Life After Hitting The Maximum

Fast forward to October. Alex needs a series of physical therapy sessions to fully recover, and the total cost is $1,500. Because the $7,000 out-of-pocket maximum has already been met, Alex pays nothing for this care. The insurance company covers the entire $1,500.

This example perfectly illustrates the power of the out-of-pocket maximum. It’s the ultimate financial guardrail that prevents a health crisis from becoming a complete financial catastrophe.

Choosing a Health Plan Based on Your Total Risk

Understanding your out-of-pocket maximum isn't just about memorizing a definition. It’s about using that number to make one of the most critical financial decisions you'll face while living abroad. This single figure helps you see past a tempting low monthly premium and truly grasp your total financial risk for the year.

This brings you to a classic crossroads. Do you go for a plan with a higher monthly premium but a low out-of-pocket maximum? Or, do you pick the low-premium plan that comes with a much scarier spending cap if things go sideways? There’s no single right answer—it all boils down to your personal health, your finances, and your tolerance for risk.

A low-premium, high-deductible health plan (HDHP) can look like a fantastic deal at first glance. But if you have a chronic condition or have a feeling you'll need more than a few doctor visits, that low monthly payment can be incredibly misleading. You could easily end up paying far more over the course of the year as you slowly chip away at a massive out-of-pocket limit.

Matching Your Plan to Your Life

On the flip side, a high-premium plan with a low out-of-pocket max offers something incredibly valuable: predictability. You pay more each month, absolutely, but you get the peace of mind that comes from knowing your potential medical spending is capped at a much lower, more manageable number. For anyone with ongoing health needs or a simple dislike for financial surprises, this is often the smarter play.

To strike the right balance, you have to do a little personal risk assessment. It’s not as intimidating as it sounds. It just means getting honest with yourself about your health and your bank account.

Your health insurance plan should match your reality. Choosing a plan based on the lowest premium is like buying a car based only on its paint color—it ignores the engine, safety features, and how it will actually perform when you need it most.

Asking the right questions is the first step. Our guide on how to compare health insurance plans walks you through this evaluation in much more detail.

Your Personal Risk Checklist

Before you sign on the dotted line for any plan, run through these crucial questions. Your answers will guide you to the right kind of coverage and reveal what that out-of-pocket maximum really means for your budget.

- Do I have any chronic health conditions? If regular doctor visits, prescriptions, or treatments are part of your routine, a plan with a lower spending cap will almost certainly be more cost-effective in the long run.

- Can my savings handle a large, unexpected bill? If having to suddenly pay several thousand dollars for a medical emergency would throw your finances into chaos, you should prioritize a lower out-of-pocket maximum, even if it means a higher premium.

- Am I planning any major life changes? Thinking about starting a family? Have a planned surgery on the horizon? You should anticipate higher medical costs and choose a plan that reflects that reality.

- Do I have access to a Health Savings Account (HSA)? This is mainly for those in the U.S. system. An HSA can be paired with an HDHP, letting you set aside tax-free money for medical costs. This can make a high-deductible plan a much more strategic and viable option.

Common Misconceptions and Costly Mistakes to Avoid

Navigating health insurance can feel like trying to find your way through a maze blindfolded. A few simple misunderstandings about your out-of-pocket maximum can lead to thousands in unexpected bills. Getting these details right is the final piece of the puzzle to using your health plan confidently and keeping your finances safe.

One of the most common—and expensive—mistakes people make is ignoring their provider network. If you see a doctor or go to a hospital that's out-of-network, the money you spend will almost never count toward your in-network out-of-pocket maximum. You could be on the hook for that entire bill yourself, without making a dent in the limit that’s supposed to protect you.

The single biggest financial mistake you can make is assuming all medical spending counts toward your out-of-pocket maximum. Always confirm a provider is in-network and a service is covered before you receive care to avoid devastating surprise bills.

Another critical point that catches people off guard is that your limit isn't a lifetime cap—it resets completely every single year.

The Annual Reset and Family Plan Rules

Your out-of-pocket maximum hits the reset button and goes back to zero on the first day of your new plan year. The thousands you spent last year won’t carry over. This is a huge deal if you’re planning for major medical expenses, because timing your procedures can make a massive difference to your wallet.

Finally, mixing up the family and individual maximums is an easy way to get a bill you never saw coming. A family plan actually has two different limits: a lower one for each person and a much higher combined limit for the entire family.

- Individual Maximum: Once one person hits this number, their own in-network, covered care is paid for at 100% by the insurance company.

- Family Maximum: This is the big number—the combined total for everyone on the plan. Once the family's collective spending hits this higher limit, all covered in-network care for every single person on the plan is paid for by the insurer for the rest of the year.

Think of it this way: if one person has a major surgery and meets their individual maximum, their costs are covered. But the other family members still have to pay their own costs until the larger family maximum is reached. Understanding that distinction is key to avoiding the shock of getting a bill you thought was already taken care of.

Frequently Asked Questions

When you start digging into the details of an out-of-pocket maximum, some very practical questions tend to pop up, especially if you have a family or you’re thinking about switching jobs. Let's tackle some of the most common ones.

What Is The Difference Between an Individual and a Family Out of Pocket Maximum?

This is a fantastic question because it trips up a lot of people. A family plan actually has two separate limits working at the same time: an individual maximum and a family maximum.

Here’s how it works. Once a single person on the plan—let's say your daughter—hits her individual limit through her own medical costs, the insurance company starts paying 100% for her covered, in-network care for the rest of the year. She’s all set.

But—and this is the important part—the rest of the family still has to pay their own way. The bigger family maximum only kicks in when the combined eligible spending of everyone on the plan reaches that higher number. Once that happens, the insurance company covers everyone on the plan at 100%.

Does My Out of Pocket Maximum Reset if I Change Jobs Mid-Year?

Yes, almost always. When you switch jobs and enroll in a new health insurance plan, your out-of-pocket maximum resets to zero. That’s a tough pill to swallow, but the money you spent toward your old plan’s limit doesn't follow you.

This is true even if your new company uses the exact same insurance provider, like Blue Cross or Cigna. Since it’s a different group plan, you’re starting over from scratch. It’s a huge financial detail to factor in when you're planning a career move.

It's worth repeating: even after you've hit your out-of-pocket max, you're not done paying for everything. You'll still have to cover your monthly premiums, any care you get out-of-network, and services your insurance company decides aren't medically necessary.

Navigating the world of international health insurance can feel overwhelming, but you don’t have to figure it all out on your own. The experts at Expat Insurance live and breathe this stuff. We specialize in finding the perfect plan for your life abroad, making sure your financial safety net is truly secure. Get a free quote today and find the right coverage for your needs.