December 28, 2025

•

5 min read

Travel Insurance vs Health Insurance: Which Is Best for Living Abroad?

Travel insurance vs health insurance: compare coverage, costs, and scenarios to pick the right global plan. (travel insurance vs health insurance)

It all boils down to two things: your purpose for being abroad and how long you plan to stay.

At its core, travel insurance is built for short-term trips. Think of it as your safety net against unexpected travel hiccups and medical emergencies while you're on vacation. In contrast, international health insurance is designed for the long haul, providing comprehensive medical care for anyone who is living or working in another country.

Choosing Your Global Insurance Coverage

Figuring out which of these you need is the first, and most important, decision for anyone spending time outside their home country. Travel insurance is for a vacation or a business trip. International health insurance is what you'll rely on as your primary healthcare plan when you're an expat.

This distinction is pretty clear when you look at the numbers. The global travel insurance market is a big one, valued at around USD 27.0 billion and growing. But the international health insurance market is even larger simply because it's covering the long-term, day-to-day healthcare needs of the entire global expat community.

Getting their core functions straight in your head is crucial before you pack your bags or book that one-way ticket.

Travel Insurance vs International Health Insurance at a Glance

A quick side-by-side comparison makes their different roles crystal clear. Travel insurance is temporary and kicks in when something specific goes wrong. An international health plan is continuous, designed to handle everything from your annual check-up to major medical events. You can dive deeper into what is international health insurance in our detailed guide.

To make it even simpler, here's a table breaking down the essentials.

| Feature | Travel Insurance | International Health Insurance |

|---|---|---|

| Primary Purpose | Covers trip cancellations, lost luggage, and medical emergencies for a specific trip. | Provides ongoing medical care, including routine check-ups, chronic conditions, and emergencies. |

| Duration | Limited to the length of a specific trip (e.g., 30, 60, or 90 days). | Annual, renewable policies designed for long-term residence abroad (12+ months). |

| Medical Coverage | Focuses on emergency medical treatment to stabilize you and often get you back home. | Comprehensive inpatient, outpatient, wellness, dental, and vision benefits. |

| Geographic Scope | Covers a specific destination or region for the duration of one trip. | Offers broad coverage areas (e.g., Worldwide excluding the USA) for continuous care. |

Ultimately, the right plan is entirely dependent on your situation. A two-week holiday in Spain has completely different insurance needs than a three-year work assignment in Singapore. Once you understand these core distinctions, you can make sure you have the right protection for whatever journey you're on.

Digging Into Core Coverage and Key Exclusions

The real difference between travel and health insurance isn't in the marketing headlines—it's buried in the fine print. You have to understand that one is built to patch you up after a crisis and get you home, while the other is designed to manage your overall health while you live in a new country. Getting this wrong can leave you with devastating gaps in your coverage.

Travel insurance is laser-focused on acute, unforeseen medical emergencies. Think of a sudden case of food poisoning, a scooter accident, or a broken arm from a fall. The goal of a travel policy's medical benefit is stabilization—giving you the care you need to be well enough to fly back home, where your regular health insurance can take over.

International health insurance, on the other hand, provides broad-spectrum medical care. It's meant to function just like your primary health plan back home, but with a global footprint. This means it covers emergencies, but also all the routine and preventative care that keeps you healthy throughout the year.

Medical Benefits: A Tale of Two Philosophies

In practice, the differences in what's covered are stark. A travel plan is built on the idea that if it can wait until you get home, it's not covered. An international health plan is designed to handle it all while you're living abroad.

Here's what that looks like on the ground:

- Inpatient Care: Both will generally cover emergency hospital stays. The big difference is that an international health plan also covers planned surgeries and hospitalizations for ongoing conditions.

- Outpatient Care: This is a massive point of separation. International health insurance is designed to cover your GP visits, specialist appointments, lab tests, and prescriptions for any health concern—not just emergencies. Travel insurance almost never touches this kind of routine care.

- Wellness and Preventative Services: International health plans often include benefits for annual physicals, vaccinations, and health screenings. This is completely outside the scope of a travel policy.

- Dental and Vision: You can usually add these on to an international health insurance plan, giving you coverage for routine cleanings, fillings, new glasses, and more. You'll almost never find this in a standard travel policy.

This huge difference in scope is reflected in the policy limits. Travel medical coverage often provides emergency limits between USD 50,000 to USD 250,000 per trip, often with strict sublimits. Meanwhile, comprehensive international private medical insurance (IPMI) plans for expats offer annual limits anywhere from USD 500,000 to unlimited.

The All-Important Issue of Pre-Existing and Chronic Conditions

This is probably the most misunderstood—and most dangerous—exclusion in travel insurance. Pre-existing conditions are any medical issues you had before your trip started, like diabetes, asthma, high blood pressure, or a previous heart condition.

Key Takeaway: Standard travel insurance policies almost universally exclude coverage for pre-existing and chronic conditions. If you rely on one for long-term residency, a claim for any related medical issue will likely be denied, leaving you to foot the entire bill.

This is where the travel insurance vs health insurance debate becomes most critical for expats. If you're living abroad and have a flare-up of a chronic illness, a travel plan will almost certainly not cover your treatment. An international health plan, however, is built for exactly this scenario. With proper underwriting, it provides continuous coverage for managing these conditions, including your regular doctor visits and prescription refills.

Our guide to the best travel medical insurance can help you find policies that offer some coverage for the acute onset of a pre-existing condition, but this is a limited, emergency-only benefit and is absolutely not a substitute for comprehensive health insurance.

Comparing Policy Duration, Portability, and Geographic Limits

How long your coverage lasts and where it actually works are two of the most critical questions in the travel insurance vs. health insurance debate. The answers get right to the heart of how these policies are designed: one is a temporary fix for a specific trip, while the other is built for a continuous, mobile lifestyle.

Getting this wrong can leave you with massive, unexpected gaps in your coverage right when you need it most.

Travel insurance is tied directly to the dates of your itinerary. You buy a policy for a fixed window of time—maybe 14 days, 30 days, or up to 180 days if you're on a longer jaunt. The moment your trip is over and you're back home, that coverage evaporates.

This trip-by-trip structure is perfectly fine for a standard vacation. But it's a huge liability for anyone living abroad long-term. Trying to string together a series of short-term travel policies is a recipe for disaster, leaving you uninsured between trips or if your plans suddenly shift.

The Limits of Trip-Based Coverage

A travel policy's duration is rigid. If you decide to extend your stay, you can't just call up and add a few more weeks to your plan. You'll likely have to buy an entirely new policy, which could mean resetting your deductible and facing new underwriting for any health issue that popped up during your initial stay.

This creates a seriously precarious situation for long-term residents.

A key risk of using travel insurance for long-term stays is the lack of portability. The policy is designed to get you well enough to return to your home country for further care, not to follow you as you move between different countries or establish a new base.

This is a crucial distinction for anyone whose life isn't defined by a single return ticket. Digital nomads, for example, need coverage that moves with them. Our guide on health insurance for digital nomads digs into the solutions built for this exact lifestyle, offering continuous protection that crosses borders seamlessly.

The Power of Annual, Renewable Plans

International health insurance is built on a completely different foundation. These are annual, renewable policies designed for continuous, long-term coverage. As long as you pay your premiums, your plan stays active, giving you seamless protection whether you're in your new country of residence, traveling for work, or visiting family back home.

This portability is a core feature. Instead of being tied to a single trip, your coverage is defined by a geographic "area of cover." You can customize this to fit your life:

- Worldwide: The most comprehensive option, covering you in literally any country.

- Worldwide Excluding the USA: A very popular and more affordable choice, as it carves out the notoriously high costs of US healthcare.

- Specific Regions: Some insurers offer plans limited to Europe, Southeast Asia, or other defined areas to bring premiums down even further.

This structure gives you the freedom to get care wherever you are within your chosen zone. You could see a specialist in Germany, get a routine check-up in Thailand, and still be covered for an emergency during a weekend trip to Brazil—all under one consistent policy.

For an expat, this means your health plan is as mobile as you are. It provides a stable, predictable safety net, no matter where your life or work takes you next.

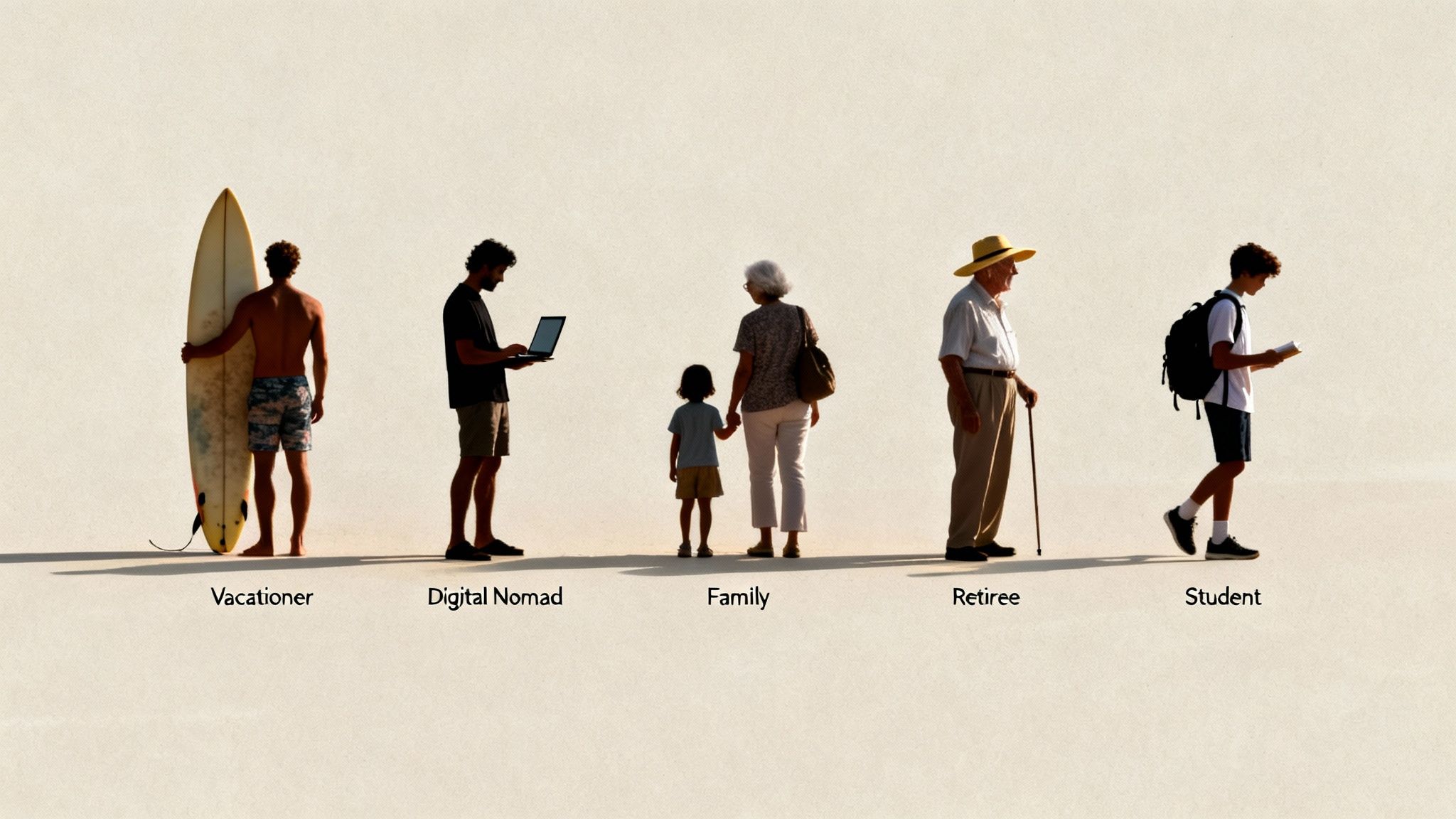

Putting It All Together: Real-World Scenarios

Theory is one thing, but the real test in the travel insurance vs. health insurance debate comes down to your life and your plans. The best way to figure out which policy you really need is to walk through a few common scenarios. You'll probably see a bit of yourself in one of these profiles.

Let's break down five classic examples of people living and traveling abroad to see which insurance makes sense for them.

Scenario 1: The Two-Week Vacationer in Italy

Meet Sarah. She's 30 and jetting off for a two-week dream holiday to Rome and the Amalfi Coast. She's not worried about check-ups or chronic conditions; her main concerns are the classic travel headaches and sudden medical emergencies.

- Her Priorities: Coverage for a cancelled flight, lost bags, and emergency medical care if she gets sick or has an accident.

- What Could Go Wrong: A sudden case of food poisoning lands her in a local hospital, she sprains an ankle hiking near Positano, or her passport gets stolen.

- The Bottom Line: She just wants an affordable safety net for her trip, not a pricey plan with benefits like long-term prescription coverage she'll never use.

Recommendation: This one's easy. Travel Insurance is the perfect fit. A solid travel policy covers her biggest risks for the exact dates she's away, giving her peace of mind without the cost and complexity of a full-blown health plan.

Scenario 2: The Digital Nomad in Southeast Asia

Next up is Ben, a freelance developer living the nomad life. He plans to spend the next six to eight months working from Thailand, Vietnam, and Bali, hopping to a new spot every couple of months. He needs medical coverage that moves with him.

- His Priorities: Continuous, portable medical insurance that works across borders for both emergencies and minor health issues.

- What Could Go Wrong: A serious motorbike accident, contracting a tropical illness like dengue fever, or needing to see a specialist for a nagging health issue. A travel policy with a 90-day limit would leave him completely exposed after his first stop.

- The Bottom Line: He's looking for a cost-effective annual plan that gives him reliable access to doctors and hospitals without the frills of a corporate package.

Recommendation: International Health Insurance is non-negotiable for Ben. A "Worldwide excluding USA" plan is his best bet, providing seamless protection as he moves. It means he can get treated at a top hospital for a serious injury or just visit a local clinic for a check-up—things a travel policy would never touch.

Stacking short-term travel insurance policies is a huge gamble for anyone living abroad for more than a few months. It creates massive coverage gaps. An annual international health plan is the only real way to stay protected.

Scenario 3: The Corporate Expat Family in Dubai

Let's look at the Chen family. They're moving from the UK to Dubai for a three-year corporate assignment with their two young kids. They'll need regular pediatric check-ups and vaccinations. On top of that, Mrs. Chen has a managed thyroid condition that requires ongoing monitoring.

- Their Priorities: Comprehensive family healthcare, from routine doctor visits and dental work for the kids to managing a pre-existing condition and accessing a network of English-speaking specialists.

- What Could Go Wrong: The kids getting sick, struggling to manage a chronic illness in a new healthcare system, or simply needing a trusted family doctor.

- The Bottom Line: With an employer likely subsidizing the cost, their focus is on getting a high-quality, comprehensive plan that leaves no stone unturned.

Recommendation: A robust International Health Insurance plan is the only real choice here. They need a policy that explicitly covers pre-existing conditions and offers strong outpatient benefits for their children's routine care. Travel insurance wouldn't cover a single one of their day-to-day medical needs.

Scenario 4: The Retiree in Mexico

David and Susan are retiring to Lake Chapala, Mexico. Now in their late 60s, their top priority is knowing they can access excellent private healthcare for anything that comes up, from preventative screenings to major surgeries. They'll live in Mexico full-time but want to visit family in the US occasionally.

- Their Priorities: Reliable coverage for age-related health issues, managing chronic conditions, and any major medical events that might occur.

- What Could Go Wrong: A sudden heart attack, needing a joint replacement, or requiring ongoing cancer treatment. These are high-cost situations that are miles beyond what any travel policy could handle.

- The Bottom Line: They're on a fixed income but aren't willing to compromise on health security. They need a balance of comprehensive benefits and a manageable annual premium.

Recommendation: International Health Insurance is an absolute must. They should look for a plan with excellent coverage in Mexico that also includes an option for short-term emergency coverage when they travel back to the United States. This gives them a complete healthcare solution for their new life.

Scenario 5: The Student Abroad in Spain

Finally, we have Maria, a 21-year-old American spending her academic year in Madrid. The university and her student visa have strict health coverage requirements. She needs a plan that ticks all the boxes, covering emergencies and basic healthcare for her 10-month stay.

- Her Priorities: A visa-compliant plan that covers emergency care and allows her to see a doctor for common illnesses like the flu.

- What Could Go Wrong: A sports injury from a pickup soccer game, needing a prescription filled, or having to see a specialist.

- The Bottom Line: Being a student, her budget is tight. She needs an affordable plan that meets all the legal and university rules.

Recommendation: This calls for a Hybrid Approach or a Student-Specific International Health Plan. A standard travel policy won't cut it for a visa. Luckily, many international health insurers offer affordable plans designed specifically for students abroad. They provide much more than just emergency care and are built to satisfy visa requirements.

To make this even clearer, here's a quick summary table matching these profiles to their ideal insurance.

Insurance Needs by Expat Profile

This table helps you quickly identify the right insurance based on your specific situation.

| Expat Profile / Scenario | Primary Need | Recommended Insurance Type | Key Consideration |

|---|---|---|---|

| Two-Week Vacationer | Trip protection & emergency medical | Travel Insurance | Coverage is tied to the trip dates and focuses on unforeseen events, not routine care. |

| Digital Nomad (6+ Months) | Continuous, portable medical care | International Health Insurance | Needs a policy that covers multiple countries and is not limited to a short duration. |

| Expat Family | Comprehensive family healthcare | International Health Insurance | Must cover routine check-ups, pediatrics, and pre-existing/chronic conditions. |

| Retiree Abroad | Long-term, major medical coverage | International Health Insurance | Focus on high benefit limits, chronic care, and access to quality private hospitals. |

| Student Abroad (Long-Term) | Visa compliance & basic healthcare | Student International Health Plan | Needs to meet specific legal requirements while remaining affordable for a student budget. |

Ultimately, choosing the right plan comes down to honestly assessing your lifestyle, health needs, and how long you plan to be away from home. One size definitely does not fit all.

Costs, Claims, and Networks: The Day-to-Day Differences

Beyond what's covered on paper, the practical side of things—how you pay for care, get reimbursed, and find a doctor—is where you'll feel the biggest difference between travel and health insurance. It's the contrast between a pay-first, claim-later model built for emergencies and a seamless system designed for ongoing healthcare.

Understanding these financial and logistical differences is crucial. They can mean the difference between a minor inconvenience and a major financial crisis when you're far from home.

The pricing alone tells you everything you need to know about their intended purpose. Travel insurance is priced on a per-trip basis. The cost hinges on your age, how long you'll be gone, and where you're headed. A two-week getaway to Mexico might only set you back a hundred dollars, making it a perfectly affordable short-term fix.

International health insurance, on the other hand, is priced annually, just like the health plan you'd have back home. Premiums are calculated based on your age, the coverage level you select (like inpatient-only versus a comprehensive plan), your deductible, and the geographical area you need coverage in. This structure is built for the long haul, serving as your primary health plan while living abroad.

Decoding the Claims Process

How your medical bills get paid is probably the most glaring difference between the two. It's a classic showdown between "pay-and-claim" versus "direct billing," and the one you have can have massive financial consequences.

Most travel insurance policies are built on a pay-and-claim model. For the majority of medical issues, you're expected to pay the clinic or hospital out-of-pocket first. Then, you gather your receipts and paperwork to file a claim for reimbursement later. This works fine for a minor doctor's visit, but it can quickly become a financial nightmare in a real emergency.

Imagine having a serious accident and being told you need to put down a $20,000 deposit before the hospital will admit you. For most people, that's simply not possible. This is the single biggest risk of relying on a pay-and-claim system for anything more than a small incident.

International health insurance flips this script entirely. It's built around direct billing networks. Insurers establish partnerships with hospitals and clinics across the globe, allowing the medical facility to bill them directly. You just show your insurance card, cover your deductible or co-pay, and the insurance company handles the rest of the bill. This system removes the terrifying prospect of having to front huge sums of money for major medical care.

This fundamental difference is tied to what each policy is designed to do. Travel insurance claims are mostly for trip cancellations and unexpected medical emergencies. In stark contrast, international health insurance claims are dominated by routine doctor's visits and planned hospital stays. It's why industry experts often recommend that new expats secure a proper international health plan 30 to 45 days before departure—to ensure continuous coverage from day one.

Why Provider Networks Matter

The idea of a "provider network" is the backbone of international health insurance, but it's a concept that's mostly missing from the travel insurance world. A network is simply a list of hospitals, specialists, and clinics that the insurer has already vetted and set up a direct billing arrangement with. For an expat, this is a huge deal.

- Quality Assurance: Facilities in the network have been checked out by your insurer, giving you some peace of mind that you're going to a reputable place.

- Easy Access: Instead of frantically Googling "best doctor in Lisbon" during a crisis, you can just pull up your insurer's approved list.

- Painless Payments: As we covered, direct billing means no massive upfront payments and no stressful reimbursement paperwork.

Travel insurance doesn't really have a formal network. Sure, their 24/7 assistance line can point you to a nearby hospital in an emergency, but they don't have those integrated, cashless relationships. You're free to choose any provider, but you're also the one responsible for footing the bill first. For anyone actually living abroad, the curated access and financial simplicity of a health insurance network makes navigating a foreign healthcare system infinitely easier.

A Decision-Making Checklist for Expats

Figuring out whether you need travel insurance or a full-blown international health plan really comes down to asking the right questions about your life abroad. Instead of getting bogged down in policy jargon, this simple checklist can cut through the noise and point you in the right direction.

Answering these questions honestly isn't just about ticking boxes; it's about painting a realistic picture of what you'll actually need on the ground.

Key Questions to Ask Yourself

Work your way through these points. Your answers will quickly reveal if your needs are temporary and emergency-focused, or if you require something more permanent and comprehensive.

-

How long will you be abroad? If you're talking about a few weeks or even up to three months for a single trip, travel insurance usually does the trick. But if you're planning to live somewhere for six months, a year, or longer, you absolutely need the continuous, renewable coverage that only an international health plan provides.

-

Do you have any pre-existing or chronic conditions? This is a massive fork in the road. If you need regular care for conditions like diabetes, asthma, or high blood pressure, travel insurance is not a solution. Only a proper international health insurance policy is designed to cover the routine check-ups, specialist visits, and prescriptions required to manage these ongoing conditions.

-

Will you need routine medical care? Think about your typical year back home. Do you get an annual physical? See a specialist for a nagging issue? Go for dental cleanings? Travel insurance covers none of that. If you want the ability to get preventative care and handle non-emergency medical needs, an international health plan is your only real option.

Making the right choice is fundamental to your financial security and well-being abroad. The wrong policy can lead to denied claims for routine care, leaving you with significant out-of-pocket expenses for predictable medical needs.

Budget and Next Steps

Finally, you have to consider the financial side of things.

- What is your budget for premiums vs. potential costs? Travel insurance has a very low upfront cost, but it can leave you exposed to astronomical bills for anything that isn't a clear-cut emergency. International health insurance has a higher monthly premium, but in return, it gives you a robust safety net that protects you from truly catastrophic medical expenses.

The best next step is often to chat with a specialist broker. They can pull personalized quotes based on your answers and offer transparent advice to help you lock in the right protection for your new life as an expat.

Frequently Asked Questions

Digging into the world of global insurance always brings up a few specific "what-if" scenarios. Here are some of the most common questions we hear when people are weighing travel insurance against international health insurance.

Can I Use Travel Insurance For a Visa Application?

The short answer is almost always no. Most countries that require proof of health coverage for long-term visas—think student, work, or residency permits—will reject a standard travel insurance policy out of hand.

Immigration officials want to see that you have access to comprehensive, ongoing medical care, which is exactly what international health insurance provides. A travel policy is built for temporary emergencies, not for setting up life in a new country. Submitting one is a common and surefire way to get a visa application denied. Always triple-check the specific insurance requirements for your destination; they'll spell out that you need a plan covering both emergency and routine healthcare for your entire stay.

What Happens If My Trip Becomes a Long-Term Stay?

This happens all the time, especially for digital nomads or anyone whose travel plans are fluid. One minute you're on a three-month trip, the next you're looking for an apartment. The moment that shift happens, your travel insurance becomes dangerously inadequate. You can't just keep extending a travel policy forever and expect it to cover you properly.

Crucial Point: Once you go from being a "traveler" to a "resident" in a new country, you absolutely must switch to an international health plan. Sticking with travel insurance leaves you exposed, with zero coverage for routine check-ups, managing pre-existing conditions, or any non-emergency medical needs.

The best move is to get an international health plan in place as soon as you decide to stay long-term. This prevents any scary gaps in your coverage and ensures you have the right protection for your new life abroad.

Does International Health Insurance Cover Me Back Home?

Yes, this is one of the most valuable features of a good international health plan. Most policies include some level of coverage for when you visit your home country, giving expats a ton of flexibility. Typically, you'll see benefits for short-term visits home, often for a period like 90 or 180 days per policy year.

This means you can get emergency medical care if something unexpected happens while you're visiting family or friends. Some of the more premium plans even cover elective treatments back home. It's a critical piece of the puzzle that makes your health coverage as mobile as you are. Just be sure to confirm the specific home country rules and duration limits with your provider before you travel.

At Expat Insurance, we live and breathe this stuff. Our job is to help you cut through the confusion and find the right global health plan for your situation. Our expert advisors offer clear, honest guidance and personalized quotes from over 65 insurers, making sure you're properly protected, no matter where you decide to call home. Get your free quote today!