January 11, 2026

•

5 min read

What Is Coinsurance in Health Insurance Explained for Expats

What is coinsurance in health insurance? This guide explains how it works with clear examples, helping expats understand and manage their medical costs abroad.

Let's cut through the jargon. Coinsurance is simply the percentage of a medical bill you have to pay after you've hit your annual deductible. Think of it as your insurance company saying, "Okay, you've covered the first big chunk of costs for the year. Now, let's split the rest."

Decoding Your Health Insurance Policy

Trying to understand your health insurance policy can feel like learning a new language, especially when you're an expat figuring out a totally different country's healthcare system. Coinsurance is a huge piece of that puzzle, and it has a direct impact on your wallet.

Unlike a copay, which is a flat fee, coinsurance is a percentage. You'll often see it written as an 80/20 split. In that scenario, once your deductible is paid, your insurer covers 80% of the bill, and you're responsible for the remaining 20%.

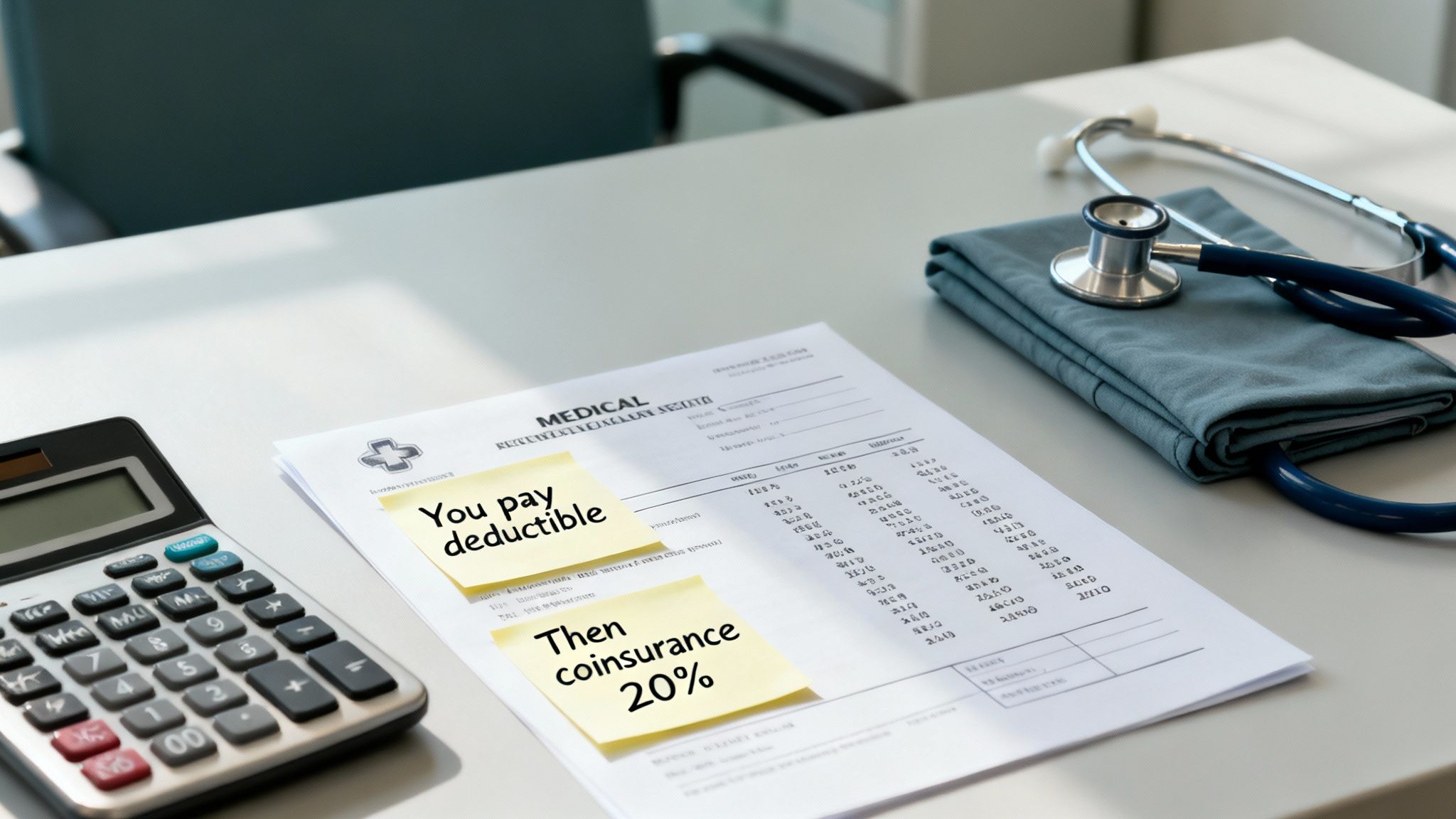

But here's the critical part: this cost-sharing only kicks in after you've paid your plan's deductible in full. Until you reach that number, you're usually on the hook for 100% of your medical bills. After that, coinsurance dictates how you and your insurer split the costs for the rest of the year—right up until you hit your out-of-pocket maximum.

The Core Components of Cost Sharing

To really get how coinsurance works, you need to see how it fits in with the other key terms on your policy. Each one is a different way you chip in for your healthcare. Getting them straight is the first step to avoiding nasty surprises on your medical bills.

Think of it like this: your deductible is the first financial hurdle you have to clear. Once you're over it, coinsurance determines the pace you run for the rest of the race, sharing the effort with your insurer.

These terms all work together to define how much you'll actually spend in a given year. Understanding how they interact is fundamental for any expat trying to manage an international health plan. To make it a bit clearer, here's a quick breakdown of the terms you'll see most often.

Key Health Insurance Terms at a Glance

Here is a quick comparison of the most common cost-sharing terms you'll find in an expat health insurance plan.

| Term | What It Is | When You Pay It |

|---|---|---|

| Deductible | The fixed amount you must pay out-of-pocket for covered services before your insurance starts paying. | At the beginning of your policy year, before cost-sharing kicks in. |

| Coinsurance | A percentage of the cost for covered services that you pay after your deductible has been met. | After your deductible is met, for most medical services. |

| Copay | A fixed fee you pay for specific services, like a doctor's visit or a prescription. | At the time of service, often before the deductible is met. |

| Out-of-Pocket Maximum | The absolute most you will pay for covered services in a policy year, including all other cost-sharing. | Once this limit is reached, your insurer pays 100% of covered costs. |

Getting a handle on these four terms puts you way ahead of the game. They form the foundation of how your plan's costs are structured.

How Coinsurance Works with Real-World Scenarios

Knowing the definition of coinsurance is one thing, but seeing it play out with real numbers is where the concept really clicks. The key thing to remember is that this percentage split only starts after you've paid your annual deductible in full.

Let's walk through a couple of practical scenarios to see exactly how these costs add up. To make it simple, we'll imagine your international health plan has a fairly common structure:

- A $2,000 annual deductible.

- An 80/20 coinsurance split (your insurer pays 80%, you pay 20%).

- A $7,000 out-of-pocket maximum for the year.

For these examples, let's also assume it's the beginning of the year and you haven't paid a cent toward your deductible yet.

Scenario 1: An Unexpected Emergency Room Visit

You're hit with a sudden illness and need to visit the emergency room in your new country. The total bill for the visit—including all the tests and treatments—comes to $3,500. So, who pays what?

First, you have to tackle that deductible. Since the bill is more than your $2,000 deductible, you'll pay that amount out of pocket. Just like that, your deductible for the entire year is met.

Now we look at the leftover amount, which is $1,500 ($3,500 total bill - $2,000 deductible). This is where your 80/20 coinsurance kicks in.

- Your insurer pays 80% of the remaining $1,500, which is $1,200.

- You pay 20% of the remaining $1,500, which is $300.

Your Total Cost: You pay the $2,000 deductible plus your $300 coinsurance share, adding up to $2,300 out of your own pocket.

Scenario 2: A Scheduled Surgery

Later in the same year, you need a minor, non-emergency surgery. The total bill for the procedure comes to a hefty $10,000.

The good news? You already paid your $2,000 deductible during that ER visit, so you don't have to worry about it again this year. The coinsurance split applies to the entire $10,000 bill from the get-go.

- Your insurer covers 80% of the bill, which is $8,000.

- You are responsible for the remaining 20%, which comes to $2,000.

Your Total Cost: You pay $2,000 for the surgery. Your insurer handles the other $8,000.

After this surgery, you've paid a total of $4,300 toward your health care for the year ($2,300 from the ER + $2,000 for the surgery). This is still well below your $7,000 out-of-pocket maximum, so you'd continue sharing costs with your insurer for any other medical needs until you hit that cap.

Coinsurance vs Copay vs Deductible

Trying to get a handle on health insurance lingo can feel like learning a new language. It's easy to mix up terms like coinsurance, copay, and deductible—and that confusion can lead to some nasty surprises when the medical bills arrive. For an expat, nailing these differences is absolutely critical for managing healthcare costs in a new country.

Let's ditch the jargon and think about it this way.

Imagine your annual health plan is a trip to a giant amusement park. Each of these cost-sharing terms is just a different kind of fee you'll pay during your visit.

Your Health Plan as an Amusement Park

Thinking about your plan this way helps untangle what you pay and when you pay it. Each "fee" has a very specific job.

-

Deductible is the Park's Entry Fee: Before you can even get on the big rides, you have to buy a ticket to get into the park. That one-time entry fee is your deductible. It's the fixed amount you must pay out-of-pocket for medical care before your insurance plan even starts to chip in.

-

Copay is the Fixed Price for a Ride: Once you're inside, some things have a small, set price. Think of the Ferris wheel or a quick game at the arcade—you know exactly what it costs upfront. That's your copay. It's a flat fee (like $30) you pay for a specific service, such as a doctor's visit, no matter what the final bill from the doctor is.

-

Coinsurance is Your Share of Other Costs: For pretty much everything else—food, souvenirs, special event tickets—you agree to pay a percentage of the total cost. This is your coinsurance. It's the percentage (say, 20%) you're responsible for after you've paid your big entry fee (the deductible).

Key Takeaway: The deductible is your first big hurdle. Copays are small, predictable fees for certain services. Coinsurance is the percentage-based cost-sharing that kicks in only after your deductible is fully paid.

This analogy really shows you the order of things. First, you have to tackle the deductible—that big initial payment that gets you through the gates. Only after that's handled do your costs shift to smaller copays and your coinsurance percentage.

Getting a firm grasp on your deductible is the foundation for understanding the rest. For a deeper dive, you can learn more about how health insurance deductibles work and what to look for. Knowing how these three terms differ is the most important step an expat can take to predict and control their medical expenses, avoid financial shocks, and pick a plan that actually fits their life.

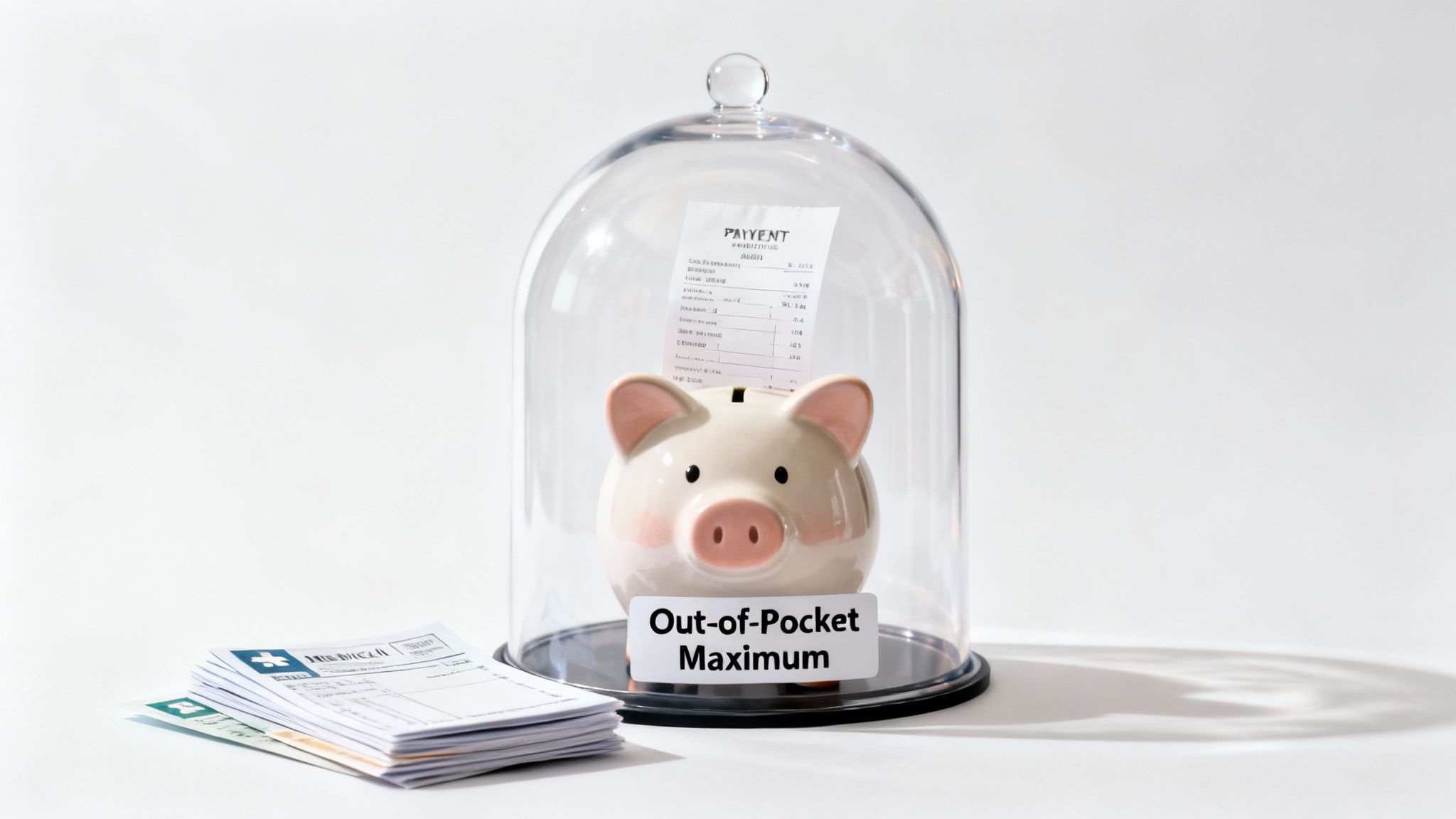

The Role of Your Out-of-Pocket Maximum

While terms like deductibles and coinsurance tell you what you'll pay for care, every health plan has a critical feature designed to protect your finances: the out-of-pocket maximum.

Think of it as the ultimate financial safety net. It's the absolute ceiling on what you will spend on covered medical care for the entire policy year. This number is arguably the most important one in your plan because it shields you from truly catastrophic bills.

Once the money you've paid for your deductible, copays, and coinsurance adds up to this limit, you're done paying for the year. Your insurer steps in and covers 100% of all eligible, in-network costs for the rest of the policy period. It's what keeps coinsurance from becoming an endless financial drain.

This protection is especially vital for expats living in countries with sky-high healthcare costs. A single unexpected surgery or serious illness could be financially devastating otherwise. Knowing your out-of-pocket maximum tells you exactly what your worst-case-scenario financial risk is for the year.

How Your Costs Add Up to the Maximum

Let's walk through a real-world example to see this safety net in action. Imagine your expat health plan has the following structure:

- Deductible: $1,500

- Coinsurance: 80/20 (Your share is 20%)

- Out-of-Pocket Maximum: $6,000

Now, let's say you need a major surgery with a total cost of $50,000. Here's the breakdown of how your payments would work:

- Meet Your Deductible: First, you pay your $1,500 deductible out of pocket. The remaining bill is now $48,500.

- Pay Your Coinsurance Share: Your 20% coinsurance on the remaining $48,500 would technically be $9,700.

- Hit the Safety Net: But you won't pay that full $9,700. Your out-of-pocket maximum is $6,000. Since you've already paid $1,500 for the deductible, you only have to pay another $4,500 in coinsurance costs before you hit your annual limit.

Your Final Bill: Your total out-of-pocket cost for the entire $50,000 surgery comes to exactly $6,000. Your insurer picks up the remaining $44,000. For any other covered medical care you need that year, your cost is $0.

This structure is what makes international health coverage work. It balances affordability with powerful financial protection, which is crucial when navigating healthcare systems abroad. To dig deeper into how this works, you can check out our complete guide on what is an out-of-pocket maximum.

How Provider Networks Impact Your Coinsurance

Figuring out what coinsurance is in health insurance is only half the battle. If you're an expat, the next big question is, "Okay, but which doctors and hospitals can I actually go to?"

The answer is hiding in your plan's provider network, and believe me, sticking to it is one of the smartest ways to keep your healthcare costs from spiraling out of control.

Simply put, a provider network is just a list of doctors, specialists, hospitals, and clinics that have a deal with your insurance company. They've agreed to give services to the insurer's members at pre-negotiated, discounted rates. When you see one of these "in-network" providers, your insurer passes those savings right along to you.

And that's where the connection to your coinsurance becomes painfully clear. Your coinsurance percentage will almost always be much, much lower when you stay in-network. For instance, a typical international plan might have a 20% coinsurance for in-network care but jump to 40% or even 50% if you go out-of-network.

The Financial Chasm Between In-Network and Out-of-Network

Going "out-of-network" just means picking a doctor or hospital that doesn't have a contract with your insurer. Since there's no pre-negotiated discount, that provider can charge their full, undiscounted rate. Your insurance plan will then turn around and make you shoulder a much bigger piece of that much bigger bill.

This isn't some minor detail buried in the fine print; it's a core strategy for how insurers manage costs. In fact, a global survey found that 70% of insurers ranked contracted provider networks as their number-one method for controlling costs, often by pairing them with different coinsurance levels.

For you as an expat, this could mean paying 10–20% coinsurance at a hospital in the network versus 30–40% at one that isn't, all after you've already met your deductible. You can dive deeper into how these global medical trends are shaping insurance plans in the WTW Global Medical Trends Survey.

Let's put some real numbers to this to see how it plays out.

Imagine you need a procedure that costs $5,000 and you've already paid your deductible for the year. With a 20% in-network coinsurance, your share of the bill is $1,000. But if you go out-of-network and your coinsurance shoots up to 40%, your bill for the exact same service doubles to $2,000.

To really drive the point home, see how choosing a provider inside or outside your plan's network drastically changes your final bill.

In-Network vs Out-of-Network Cost Example

| Cost Detail | In-Network Provider | Out-of-Network Provider |

|---|---|---|

| Provider's Billed Amount | $8,000 | $8,000 |

| Insurer's Negotiated Rate | $5,000 (Discounted) | $8,000 (No Discount) |

| Your Deductible (Already Met) | $0 | $0 |

| Your Coinsurance Rate | 20% | 40% |

| Your Share of the Bill | $1,000 (20% of $5,000) | $3,200 (40% of $8,000) |

| Total You Pay | $1,000 | $3,200 |

That's a $2,200 difference for the same procedure. The lesson here is that using the network isn't just a suggestion—it's the key to making your insurance work for you.

Practical Steps for Expats

Trying to get a handle on a new healthcare system is tough enough. A few simple habits can save you a fortune.

- Always Check the Network First: Before you book any non-emergency appointment, hop on your insurer's online portal or call their member services line. Get a list of in-network doctors and facilities in your area.

- Confirm with the Provider: When you call to make the appointment, double-check with the clinic's front desk. A simple, "Do you accept [Your Insurance Company Name]?" can save you a world of hurt later.

- Know Your Emergency Plan: In a true, life-or-death emergency, just get to the nearest hospital. Most plans have special provisions for emergency care, but you should still get in touch with your insurer as soon as it's practical to do so.

Why Coinsurance Is a Big Deal for International Plans

If you're an expat, getting your head around coinsurance isn't just about the fine print—it's a core piece of the puzzle. Insurers lean on it, especially in global plans, as a way to manage the wildly different (and often high) costs of medical care around the world. The upside for you? It helps keep your monthly premiums from skyrocketing.

Think of it as a form of shared responsibility. By asking you to cover a percentage of the bill after your deductible is met, it encourages everyone on the plan to be a bit more mindful about using healthcare services. This prevents overuse that would otherwise drive up costs for the whole group.

Local Healthcare Systems and How They Shape Your Plan

The way coinsurance is structured in an international plan is also heavily influenced by the healthcare system in your new home country. Whether a nation has a public system, a private one, or some mix of the two directly impacts how insurers design their cost-sharing. This is something you'll want to pay close attention to when looking for comprehensive international health insurance for expats.

For instance, in countries with a really strong public healthcare system, an expat plan might have higher coinsurance for treatments you choose to get outside of that public network.

For insurers, coinsurance is a balancing act. It lets them offer those big, comprehensive global networks while protecting themselves from the financial risk of unpredictable healthcare costs from one country to the next.

You'll see this cost-sharing pop up most often with outpatient care—things like specialist visits, lab work, and diagnostics. It makes sense when you look at the global picture. While more than 70% of total health spending in OECD countries is funded from public sources, there remains a significant role for private insurance and out-of-pocket payments, especially for outpatient services in many regions.

This is why it's so common to see international plans with a 10–30% coinsurance for diagnostics and doctor visits. It's a tool to help manage costs without making premiums unaffordable. For a deeper dive, the OECD has some great data on these global healthcare financing trends.

Common Coinsurance Questions Answered

Even when you've got the basics down, a few specific questions always seem to pop up when you're staring at the fine print of an international health plan. Let's tackle some of the most common ones expats ask about how coinsurance really works in practice.

Can I Find an Expat Plan with No Coinsurance?

Absolutely. Some premium international plans will offer 100% coverage after you've paid your deductible, which means your coinsurance is 0%.

Be warned, though—these top-tier plans come with a much higher monthly premium. For most expats, a policy with 10% or 20% coinsurance hits the sweet spot, giving you a great balance between affordable monthly payments and solid financial protection when you need it.

Does Coinsurance Apply to Every Medical Service?

Not always, and this is a key point to understand. Coinsurance usually kicks in for major medical services after you've met your deductible for the year.

Many plans cover preventive care—think annual check-ups or routine vaccinations—at 100%, with no cost-sharing from you at all. Other services, like a simple visit to your doctor for a minor issue, might just require a small, fixed copayment instead of activating your coinsurance.

Always check your policy's "Schedule of Benefits" document. This is your definitive guide, detailing exactly how cost-sharing applies to different types of medical care.

How Do I Track My Out-of-Pocket Costs?

Most modern insurers make this pretty easy. They'll have an online member portal or a mobile app where you can see your claims history in real-time. This is the simplest way to check how much you've paid toward your deductible and your out-of-pocket maximum.

Every time a claim is processed, your insurer will also send you an Explanation of Benefits (EOB). This document is your best friend. It breaks down exactly what the doctor billed, what the insurance company paid, and what portion you're responsible for. Reviewing your EOBs as they come in is the best habit you can build to stay on top of your healthcare spending and avoid any nasty surprises.

Navigating global health plans can feel complicated, but you don't have to do it alone. The expert brokers at Expat Insurance can help you compare plans from over 65 insurers to find the right coverage for your life abroad. Get your free, personalized quote today at https://www.expatinsurance.com.